Home Buying Checklist: Finance, Documentation & Smart Budgeting

Making a purchase of a home is a great milestone. To the majority of Indian families, it is not only a buying experience, but a financial investment. Being financially ready is less stressful and easy going whether you are intending to apply to a home loan company in Delhi or find a good home loan provider in Noida.

The following is a realistic checklist to assist you in being organised during the planning of buying a home.

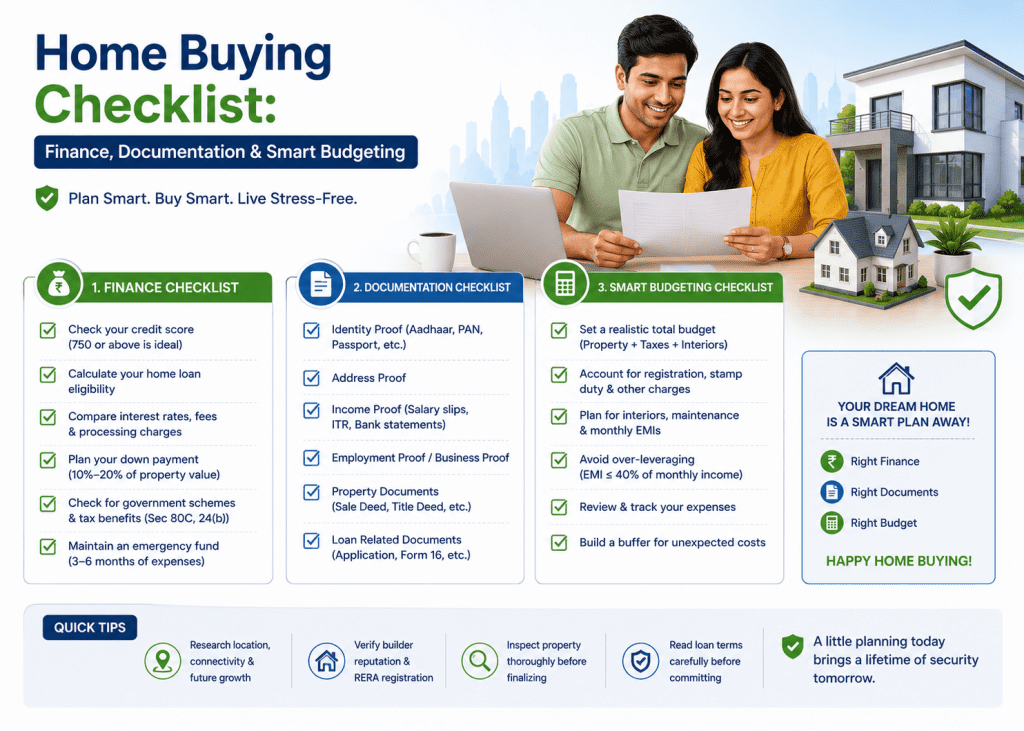

1. Get Your Financial Health in Check

Take a look at your present financial status before you apply for a loan to buy a home.

a. Credit Score: A credit score of 700 and above is preferred by most banks and NBFCs. The larger the score, the better the chances of you being approved and also bargaining a lower rate of interest.

b. Monthly Income and Expenses: This should not be higher than 40-50 per cent of your monthly revenue.

c. Loans in Progress: In case you already have an unsecured personal loan in Delhi or any other liability, consider it in repayment capacity.

These basics will help you avoid over-borrowing and guarantee that you will not choose an excessive loan amount that you will be comfortable with.

2. Decide Your Budget Wisely

Smart budgeting is not just about the calculation of the price of property. You must include:

a. Down payment (typically 10-25% of the value of the property)

b. Registration and stamp duty fees.

c. Legal and processing fees

d. Internal and changing costs.

e. Emergency savings

Financial analysts suggest maintaining a six months expenses buffer. Although you may be eligible to borrow more money from a home loan firm in Delhi, borrow what you need based on your long term plans.

3. Compare Loan Options

Take not the first offer you come across. Compare:

a. Fixed and floating interest rates.

b. Processing charges

c. Penalties of pre-payments and foreclosures.

d. Loan tenure flexibility

A large number of individuals use the home loan rates offered by a Noida-based lender to ensure they get better rates. A difference of just 0.5 in the interest rate can have an enormous effect on the amount of repayments you make in 20 years.

4. Keep Documentation Ready

Lending is secured by good documentation. The types of documents that are frequently needed are:

a. Address proof (Aadhaar), identity proof.

b. Income evidence (salary slips or ITR in case of applicants who are self-employed)

c. Bank statements (last 6 months)

d. Documents on property and sale agreement.

Lenders might ask you to provide other financial statements in case you are self-employed or borrowed some money in the form of a business loan in Delhi before. Delays are avoided by keeping everything in order.

5. Think Long-Term

A home loan is usually a 15-25-year loan. Have a vision of what you will need in the future such as education of the kids, business plans or expansion. To illustrate, when you intend to seek a business loan in Noida in the future, by keeping the repayment history of your home loan, then your credit profile will be enhanced.

Conclusion

It takes time, patience, and monetary restraint to purchase a house. Whether it is checking your credit score or documents, budgeting and more, it counts. It is organized and you will not regret having a dream home that becomes a burden.

KG Loan helps individuals to know their needs on home loans and makes a wise decision depending on their financial profile because it provides them with the necessary guidance and explanations of the home loan process.