Step-by-Step Home Loan Process in India (2026 Updated Guide)

Purchasing a house is one of the largest monetary choices in existence. A home loan can fulfill that dream for most people in India. By 2026, the procedure of acquiring a home loan will have been made more accessible and digital, although the fundamental actions will remain unchanged. When you are going to apply with a home loan company in Delhi or a home loan provider in Noida, it would help you save time and stress when you know how to do it.

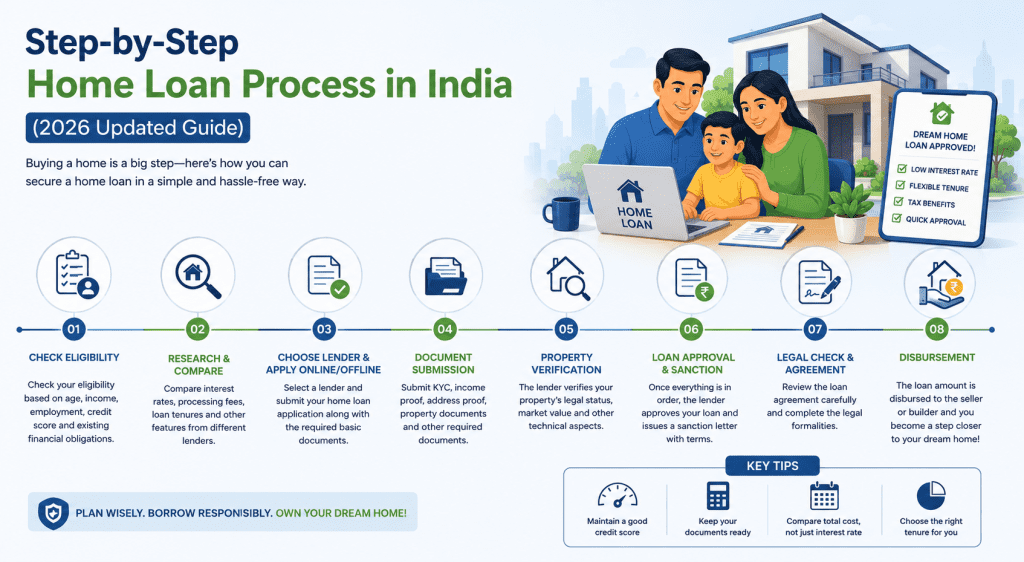

We can divide it into some steps.

Step 1: Check Your Eligibility

Ensure that you satisfy the lending requirements of the lender before you apply. Banks and the NBFCs tend to examine:

- Age (generally 21-65 years)

- Income stability

- Type of employment (self-employed or salaried)

- Credit score (preferably 700+)

In 2026, most lenders provide an online calculator to estimate their eligibility, and it is less complicated to estimate the amount of money you will be able to borrow.

Step 2: Compare Loan interests and rates.

The interest rates in India usually vary between 8 to 10 percent and this varies according to the lender and your profile. Compare:

- Floating and fixed interest rates.

- Processing fees

- Prepayment or foreclosure expenses.

- Tenure of loan (30 years in most cases)

Although you might already be aware of the possibilities such as an unsecured personal loan in Delhi, it is important to keep in mind that home loans are secured loans and they tend to attract lower interest rates because of the collateral of property.

Step 3: Documents Preparation and Submission

A very important step is documentation. Common documents include:

- Identity and address proof

- Evidence of Income (salary slips, ITR, bank statements)

- Property documents

- Employment proof

Most lenders accept digital uploads and e-KYC verification in 2026 which hastens the process.

Step 4: Application and processing of the loan.

After applying, the lender goes through your credit history and makes certain that you are genuine by doing a check of the documents submitted. They can also assess your repayment ability.

In this step, the lender puts forward a sanction letter that states:

- Approved loan amount

- Interest rate

- Tenure

- EMI amount

- Read out and accept this document.

Step 5: Verification of property and legal check-up

The lender engages in a legal and technical check of the property. This ensures:

- Clear ownership title

- No legal disputes

- Adequate construction permits.

- This is done to save you and the lender.

Step 6: Loan Disbursement

Once the loan is verified and signed the amount is disbursed. The funds could be disbursed depending on the type of property:

- In full (for resale property)

- In phases (under-construction property).

EMIs tend to start on a date of full disbursement or partial disbursement.

Conclusion

Digital tools, expedited approval and better policy have made the process of getting a home loan in India easier. The home loan application process may be done with a home loan company in Delhi, a home loan provider in Noida, or you may be considering options like a business loan in Delhi but in any case knowing every step will aid you in making the right decisions.

To those in need of a systematic approach and explanations about the home purchasing process, KG Loan will assist individuals in obtaining a better perspective on the process and will guide them in the right direction.